ENVIRONMENT

ENVIRONMENT

Thinking about the environment

The SCROLL Group will set goals in line with the following environmental activity policies for the environmental load that may occur in corporate activities,and will contribute to reducing the environmental load of the entire value chain through its business.

Environmental activity policy

(1)We will promote the provision of safe and secure products and services with less environmental impact.

(2)We will promote the reduction of waste and greenhouse gas emissions.

(3)We will promote the use of environment-friendly resources and the recycling of resources.

(4)We will promote environmental communication, such as educating employees and promoting understanding of our business partners.

(5)We will regularly verify and announce the results of our goals and promote continuous improvement of environmental performance.

CO₂ reduction targets / measures

Reduction target

The SCROLL Group aims to reduce CO₂ emissions from Scope 2 (*) by 50% or more by FY2030 compared to FY2020.

*Indirect discharge due to the use of electricity, heat, and steam supplied by other companies.

In the Group, CO₂ emissions from distribution centers and offices fall under this category.

Reduction measures

We will implement the following measures to reduce CO₂ emissions.

■Installation of solar power generation system

We are planning to install a solar power generation system in the Logistics center. We will conclude a power sales contract (PPA) with Electric Power company to promote the purchase of renewable energy generated by solar power generation systems.

■Purchasing CO₂ Free Electricity

We will proceed with efforts to purchase electricity derived from renewable energy from Electric Power company.

■Inverter control of air-conditioning cooling equipment

We will reduce the amount of electricity by introducing control equipment to the air-conditioning cooling equipment of SCL Hamamatsu Nishi.

■Switching to LED lighting

We will change the lighting in our facilities to LEDs and contribute to the reduction of CO₂.

Efforts to reduce environmental impact through business activities

We will proactively reduce the environmental burden through our business activities.

■Expansion of SDGs-related products

We will promote the development of environmentally friendly products, products that inherit Japanese traditions and technologies, and products that can contribute to society.

Goal

50% of SDGs-related products by FY2030 (apparel products)

■Reducing the amount of plastic materials used

We will promote the switch to environmentally friendly packaging materials.

Goal

65% reduction in plastic material usage by FY2030 (compared to FY2021)

■Reduction of paper usage

We will reduce the amount of paper used by reducing the number of copies and pages of the catalog and promoting the transition to the WEB catalog.

Goal

25% reduction in paper usage by FY2030 (compared to FY2021)

Disclosure based on the Task Force on Climate-related Financial Disclosures (TCFD)

The Group considers “Reducing environmental burdens” to be a materiality and has initiated a scenario analysis of the financial impact of climate change in line with TCFD recommendations. We will continue to enhance the content of our disclosures and promote initiatives toward a decarbonized society.

Governance

Recognizing climate change as one of the key issues affecting management, the Board of Directors identifies materiality and determines the direction of measures to resolve it. To promote activities to reduce environmental impact, including addressing climate change, a Sustainability Committee chaired by the Representative Director will be established in FY2022, and twice or more a year, the committee will work with business divisions to set targets, monitor the progress of the plan, and evaluate the implementation of the plan. In addition, the contents of the Committee meetings will be reported to the Board of Directors to ensure that the supervision of the Board of Directors is conducted appropriately.

Risk management

Risks are identified and assessed with the business divisions as risk owners. In addition, a “General Risk Management Activities” Office (RM Office) has been established as the office for the Internal Control Committee, and it supports responding to risks in business divisions. These activities are audited by the Internal Audit Department and reported to the Audit and Supervisory Committee and the Board of Directors. We have established a system that enables continuous monitoring by ascertaining the general risks related to business activities and the risks peculiar to the SCROLL Group.

In the future, the Sustainability Committee will work with the RM Office to identify and assess risks related to climate change issues while integrating them into company-wide risk management.

Strategy

●Analysis Process

With reference to the risk and opportunity items set forth in the TCFD recommendations, we examined the impact of climate change on our business for each segment of The Group’s main businesses: Solutions Business, Mail-order Business, E-commerce Business, and Group Jurisdiction Business. We have identified risk/opportunity items related to transitional changes in policy and market trends, as well as physical changes due to temperature increases, disasters, etc., covering the entire value chain from raw-material procurement to transportation/storage to product and service use.

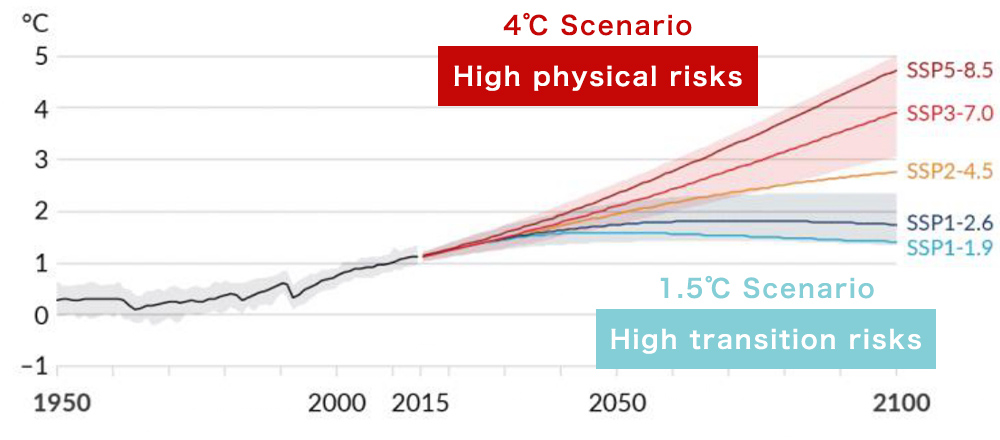

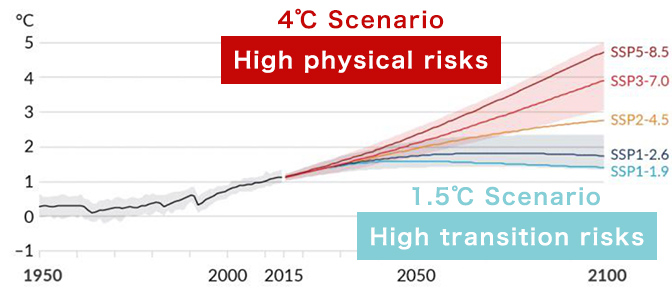

In defining the scenario groups, we have selected parameters to evaluate the financial impact of the identified transitional risks, physical risks, and opportunities from scenario groups in multiple temperature ranges. While we previously conducted analyses based on the “below 2°C scenario” and “4°C or higher scenario” in line with the recommendations, we have revised our scenario analysis by adopting the “1.5°C scenario (decarbonization transition scenario)” and “4°C scenario (high emission scenario)” as new assumptions more closely aligned with international climate goals. Through these analyses, we evaluated the impact of risk/opportunity items on the Group in 2030 and considered future response policies.

●Climate Change Scenarios

In the Definition of Scenario Groups, we refer to multiple scenarios to prepare for an uncertain future. An overview of the society envisioned under each of the “1.5°C scenario” and “4°C scenario,” as well as the names of the specific scenarios referenced, are organized in the attached table.

◆1.5°C Scenario (Decarbonization Transition Scenario)

In the “1.5°C scenario,” efforts to achieve Carbon Neutral realization are intensifying globally to suppress the effects of climate change, with the goal of limiting the increase in the global average temperature to less than 1.5°C compared to pre-industrial levels. Under this scenario, it is anticipated that countries worldwide will be required to introduce stricter regulations, implement carbon pricing (carbon taxes), and strengthen emissions trading systems to accelerate the reduction of greenhouse gas emissions. Consequently, among transitional risks, the impact of policy and legal risks may be greater than in the previous “below 2°C scenario.” For companies, a rapid transition to decarbonization technologies and renewable energy will be strongly required, and at the same time, response to these factors is predicted to have a significant impact on corporate competitiveness and market evaluation.

For our analysis, we mainly referenced the IEA NZE 2050 scenario.

◆4°C Scenario (High Emission Scenario)

This scenario assumes that climate change measures do not progress beyond current levels, resulting in a global average temperature increase of approximately 4°C by the end of this century compared to pre-industrial levels. In this scenario, physical risks such as the intensification of extreme weather conditions will become prominent, with the frequency and intensity of typhoons, torrential rain, and heatwaves expected to increase. Furthermore, with sea-level rise, the risk of flooding in coastal areas will increase, potentially having a devastating impact on people’s livelihoods and infrastructure. Thus, the “4°C scenario” is expected to bring about wide-ranging and serious impacts across society, the economy, and the natural environment.

For our analysis, we referenced the RCP8.5 scenario.

◆Global surface temperature change relative to 1850–1900

Source: IPCC Sixth Assessment Report, Working Group I, Summary for Policymakers (Provisional translation by the Ministry of Education, Culture, Sports, Science and Technology and the Japan Meteorological Agency)

Figure SPM.8, Summary for Policymakers, IPCC AR6 WGI (Provisional translation by MEXT and JMA)

◆Society Envisioned under the “1.5°C Scenario” and “4°C Scenario” and Specific Reference Scenarios

|

Decarbonization Transition Scenario (1.5℃ Scenario) |

High Emission Scenario (4℃ Scenario) |

|

|---|---|---|

| Society Envisioned | A society in which bold policies and technological innovations have been promoted to limit the temperature increase by the end of this century to 1.5°C compared to pre-industrial levels. Social changes and the strengthening of laws and regulations associated with the transition to a decarbonized society are highly likely to have a significant impact on business activities. | A society in which climate change measures do not progress beyond current levels and the global average temperature increases by approximately 4°C by the end of this century compared to pre-industrial levels. The intensification of extreme weather conditions will become prominent, and it is highly likely that torrential rain and heatwaves will have a significant impact on business activities. |

| Main Reference Scenario | IEA : NZE 2050 | IPCC : RCP8.5 |

●Main Climate-related Risks and Opportunities for The SCROLL Group

The Group has conducted an analysis of the impact of climate change on its business using the 1.5°C and 4°C scenarios in line with TCFD recommendations.

In the 1.5°C scenario, efforts toward a decarbonized society will progress, and costs will increase due to the imposition of carbon pricing (carbon taxes) based on GHG emissions. Furthermore, customer’s behavioral change may occur due to growing consumer awareness of sustainability. Based on these analysis results, we will consider the expansion of environmentally friendly products and services and the enhancement of sales promotions to respond to risks, as well as to address diversifying customer needs of consumers and businesses. The Group will also strive for reducing environmental burdens by reducing the amount of paper and plastic materials used.

In the 4°C scenario, physical damage from severe disasters such as typhoons and floods, as well as disruptions to business activities, are anticipated as risks. To address these, we will consider identifying flood risks and diversifying suppliers to enhance our responsiveness. We will also strengthen the rollout of apparel products that capture seasonal demand and emergency supplies and kits. Based on the results of this analysis, The Group views the changes brought about by climate change as medium- to long-term growth opportunities. We will aim to strengthen a highly resilient business structure and profit base by considering future response policies, based on priority, for areas that require action within The Group.

<Identified Risks/Opportunities and Response Measures>

|

Risks /Opportunities |

Drivers | Time Horizon | Target Businesses | Business Impact | Degree of Impact | Risk Response Measures | ||

|---|---|---|---|---|---|---|---|---|

| 1.5℃ | 4℃ | |||||||

| Transition Risks | Policy and Legal | Rising GHG emission prices | Medium- to long-term | All businesses |

・Higher site/logistics energy costs via carbon pricing and emissions trading ・Costs for emission credit purchases |

Low | Low |

・Install solar power at logistics centers ・Increase CO₂-free/renewable energy purchase |

| Mandates on and regulation of existing products and services | Medium-term |

Mail-order and E-commerce |

・Increased material costs by switching to alternatives due to plastic regulations | Low | Low | ・Promote eco-friendly packaging materials | ||

| Market | Changes in customer behavior | Medium- to long-term |

Mail-order and E-commerce |

・Sales decrease due to perceived insufficient environmental action or transparency | High | Medium | ・Expand environmentally friendly packaging materials | |

| Uncertainty of market signals | Medium- to long-term |

Mail-order and E-commerce |

・Reduced replacement frequency/extended usage from changed consumer environmental awareness ・Intense competition |

Medium | Low | |||

| Rising raw material costs | Medium- to long-term | All Businesses |

・Higher material prices from unstable supply ・Increased shipping costs via soaring fossil fuel prices |

Low | Low | ・Cut delivery costs via optimized inventory and leveled shipments | ||

| Reputation | Increased stakeholder concern or negative stakeholder feedback | Short- to medium-term | All Businesses |

・Lower ESG ratings/investor sentiment leading to higher financing costs and a loss of business opportunities. ・Brand damage and sales loss if response is seen as insufficient |

– | – | ・Enhance climate-related disclosures | |

| Physical Risks | Chronic | Rising average temperatures | Medium-term | All Businesses | ・Higher cooling costs at offices and logistics sites from increased usage | Low | Low | ・Reduce electricity purchase volume via PPA |

| Acute | Increased severity of extreme weather events such as cyclones, floods, and storm surges | Short-term | All Businesses |

・Facility damage costs and business stoppages; cascading sales losses from simultaneous site impact ・Lower sales via supply chain disruptions and logistics stoppages |

Low | Medium |

・Identify flood-risk areas using hazard maps ・Diversify suppliers through multi-vendor contracts ・Strengthen BCP via site diversification |

|

| Opportunities | Resource Efficiency | Use of recycling | Medium-term |

Mail-order and E-commerce |

・Build circular business model via recycling/reuse ・Enhanced corporate image and meeting customer needs |

High | Low | ・Expand eco-conscious products and businesses |

| Products and Services | Use of more efficient production and distribution processes | Medium-term |

Solutions and Group Jurisdiction Businesses |

・Lower internal costs via efficient fulfillment/BPO ・Higher revenue via eco-friendly/resource-saving solutions |

Medium | Low |

・Optimize warehouse workflows and inventory placement ・Improve delivery efficiency (CO₂ reduction via cargo consolidation) |

|

| Use of lower-emission energy sources | Medium- to long-term | All Businesses |

・Expand renewable energy use amid fossil fuel price hikes ・Long-term cost reduction and environmental contribution |

Low | Low | ・Expand clean energy use via PPA at logistics sites | ||

| Changes in consumer preferences | Short- to medium-term |

Mail-order and E-commerce |

・Higher revenue from increased demand for seasonal products due to rising temperatures/heatwaves | Medium | Medium | ・Expand apparel products capturing seasonal demand | ||

| ・increased demand for emergency supplies via extreme weather; higher sales | Low | Low | ・Strengthen sales promotion for emergency supplies | |||||

| Resilience | Ability to diversify business activities | Medium-term |

Solutions and Group Jurisdiction Businesses |

・Improved business continuity during disasters via multiple logistics sites ・Growing customer preference |

Medium | Medium | ・Strengthen BCP via site diversification | |

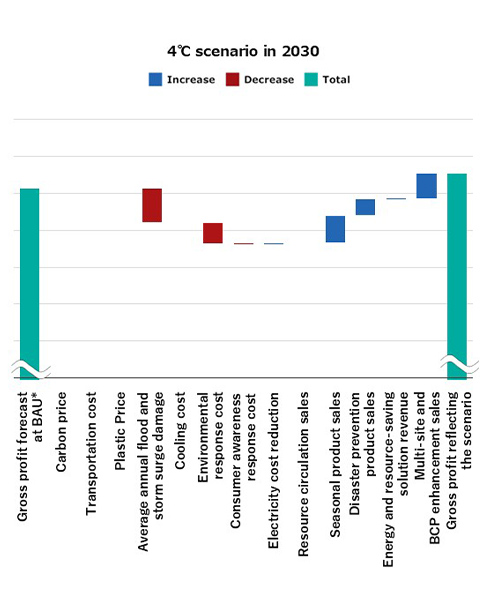

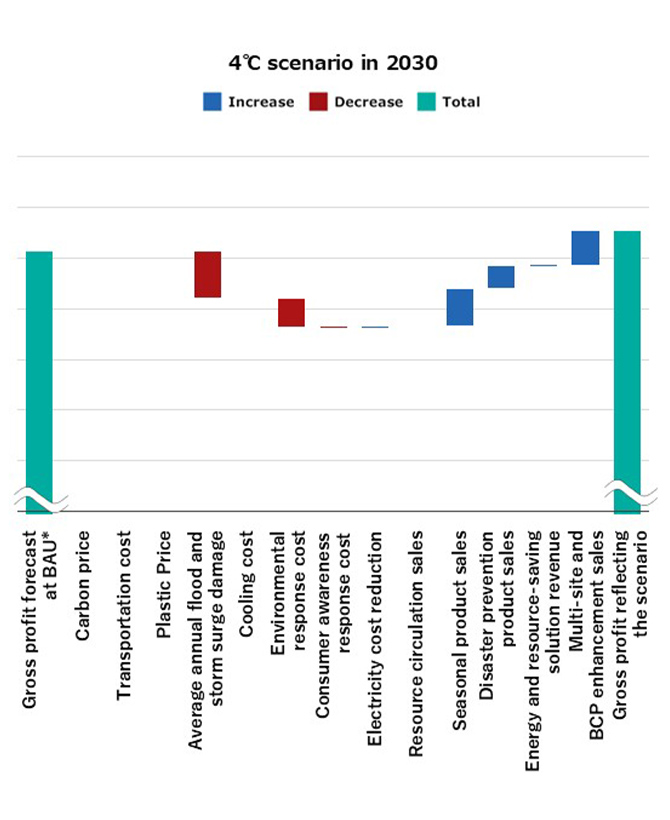

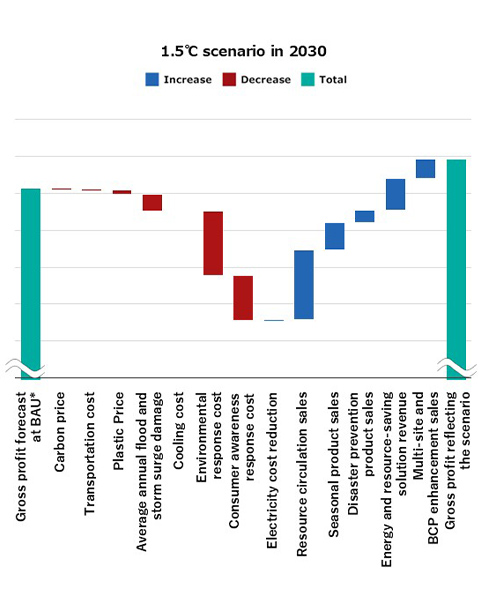

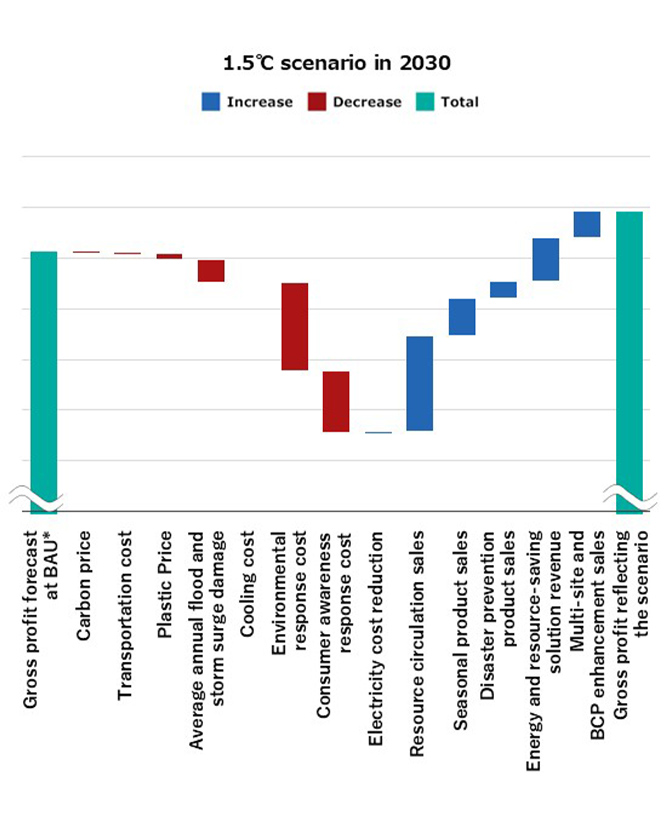

●Business Impact

Under the 4°C scenario, where climate change measures do not progress, we anticipate an expansion of opportunities such as seasonal demand and demand for strengthened BCP through site diversification. However, estimates show that overall business growth will be limited due to the impact of physical risks.

Conversely, in the 1.5°C scenario, while transition costs for environmental response are expected, we found that actively capturing business opportunities—such as resource efficiency and energy/resource-saving solutions—will absorb and minimize negative impacts. This leads to results indicating business growth that exceeds current levels.

Based on these estimates, The Group recognizes that proactive climate change initiatives minimize risks and contribute to sustainable growth. We will continue to reflect these findings in our management strategy and promote the monitoring of risks and opportunities.

*BAU Gross Profit Forecast (Business As Usual): A forecast of gross profit for 2030 based on historical performance using statistical analysis.

Indicators and Targets

●CO₂ emissions in Scope 1 and 2*

In FY 2025, Scope 1 and 2 CO₂ emissions totaled 1,632 tons.

With the goal of reducing CO₂ emissions in Scope 2, by 50% or more by 2030 compared to FY 2020, we will implement the following initiatives at our logistics facilities and office buildings, etc., which are our assets.

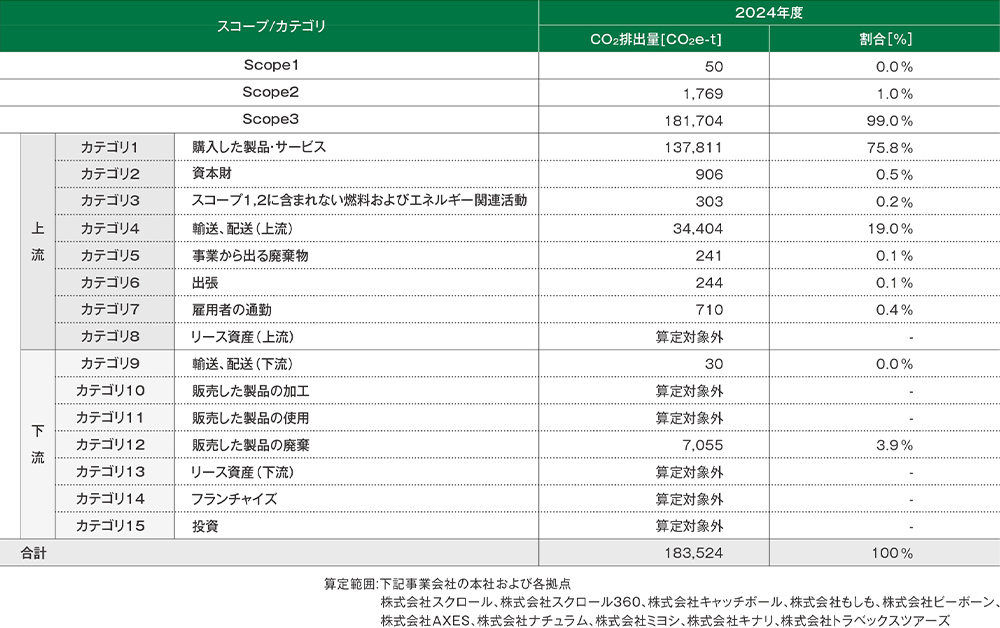

●CO₂ emissions in Scope 3*

In FY 2025, Scope 3 CO₂ emissions were 188,765 tons.

In the future, we will also consider setting targets for emissions in the value chain (Scope 3).

*

Scope 1: Direct greenhouse gas emissions by businesses themselves.

Scope 2: Indirect emissions associated with the use of electricity, heat, and steam supplied by other companies.

Scope 3: Indirect emissions besides scopes 1 and 2.

FY 2025 CO₂ Emissions (Japanese only)

●Plastic Usage

Aiming to reduce the amount of plastic materials used by 65% by FY2030 compared to FY2021 levels, we will promote the switch to environmentally friendly packaging materials.

●Paper Usage

Aiming to reduce paper usage by 25% by FY2030 compared to FY2021 levels, we will promote efficient catalog distribution, weight reduction of paper materials, and the transition to web catalogs.